College tuition keeps climbing, and choosing between 529s, Roth IRAs, or UTMAs can feel like its own elective. If you live in New York and want to stretch every federal and state tax break, this guide is for you.

Below, we break down the five strongest ways to fund a future diploma, calling out where each option excels and where it falls short—plus how new laws tip the scales.

Think of this as a roadmap, not a lecture. Short paragraphs, plain language, clear takeaways. Grab your coffee, and let’s turn sticker shock into a plan you can follow.

Why college saving in New York is different

New York gives you a built-in advantage: you can deduct up to $10,000 in 529 contributions on a joint return. That credit shows up in your refund each April and sets the Empire State apart from states that offer no break at all.

Albany adds a catch. If you tap a New York 529 for private K-12 tuition, the state will reclaim the deduction and tax the earnings. Use the account only for college costs and that risk disappears.

Cost matters, too. The direct-sold NY 529 charges a 0.11 percent expense ratio across every portfolio, so more of your money stays invested instead of paying a manager. Add that low fee to the state tax break and you start ahead of families in most other states.

Bottom line: New York’s rules can boost or bite, depending on how closely you follow them.

How we ranked the options

Good rankings should feel clear, not random. We asked one question: Which account leaves a New York family with the most spendable money when tuition arrives?

Six factors drive that answer.

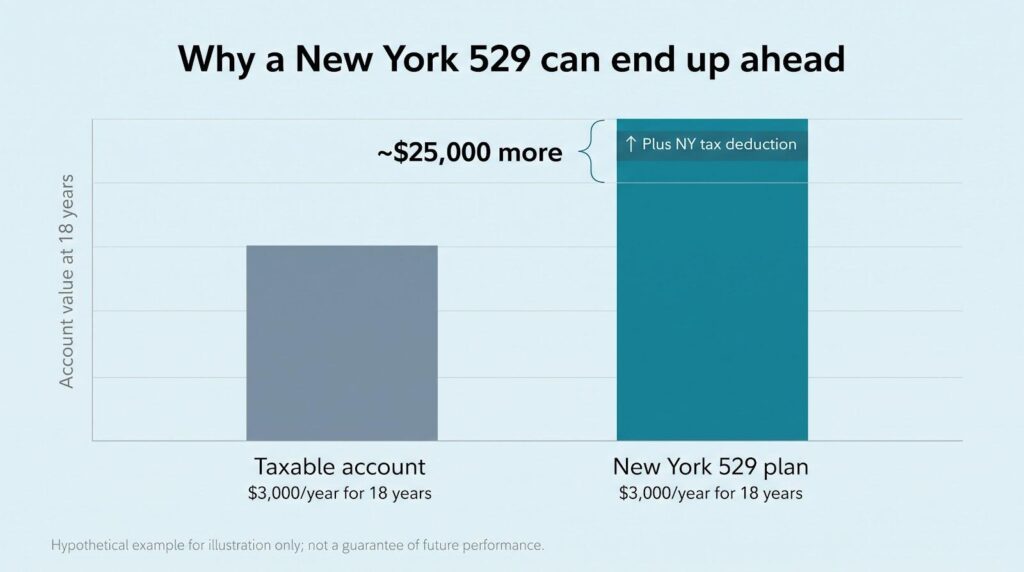

- Tax power (30 percent). A 529 withdrawal that avoids federal and state tax beats any investment tweak. Contributing $3,000 a year for eighteen years to a 529 tops a plain taxable brokerage by about $25,000 on the same contribution stream.

- Flexibility to pivot (20 percent). Rules shift, kids shift majors, life shifts. Accounts that can roll to a Roth IRA or fund a non-college goal scored higher.

- Financial-aid impact (15 percent). Parent-owned 529s barely dent FAFSA, while student assets can sink need-based aid. We built that penalty into the score.

- Cost drag (15 percent). A 0.11 percent expense ratio preserves more growth than a 1 percent adviser share.

- Growth runway (10 percent). Wider investment menus and higher contribution caps earned extra points.

- Extra perks (10 percent). State deductions, tuition guarantees, or inflation-protected interest moved an account up.

Each option earned points in every category, then we ordered them. The 529 leads the list, so seemingly safe choices sometimes land lower once the math settles.

1. 529 college savings plans: your prime engine

A 529 is the closest thing to rocket fuel for college funding. Earnings grow tax-free, and withdrawals for qualified education costs stay tax-free. New York adds a deduction on the first $10,000 you contribute each year as a married couple, cutting about $685 from your state return and freeing cash for the next deposit.

Cost control counts, too. The direct-sold NY 529 carries a 0.11 percent expense ratio across every portfolio, one of the lowest in the country. Low fees keep more of your dollars invested rather than paying a manager.

Flexibility has improved. Under SECURE 2.0, any leftover balance can move to the beneficiary’s Roth IRA, up to $35,000 over a lifetime, once the 529 is at least 15 years old and you follow the annual Roth cap. That option removes the worry of “what if my child skips college?”

Numbers tell the story. Eighteen years of steady $3,000 deposits leave a 529 roughly $25,000 ahead of an identical taxable account. Add the New York deduction each spring and the gap widens.

One caution: New York will claw back earlier deductions if you use the account for K-12 tuition, even though federal rules allow up to $10,000 a year for that purpose. Many parents open a second, out-of-state 529 for private-school bills while keeping the home-state plan focused on college.

One go-to out-of-state example is Illinois’s Bright Start 529.

ISS Market Intelligence puts Bright Start’s average asset-based fee at 0.24 percent, roughly half the 0.49 percent median for all 529 plans, and Morningstar awarded the plan a Gold rating in its 2025 review.

Those numbers show you can sidestep New York’s K-12 clawback, skip adviser mark-ups, and still keep costs and oversight firmly on your side.

Need a savings target? Enter your child’s age in the free college savings calculator to see the monthly number that meets your goal.

Bright Start College Savings Calculator Tool Screenshot

Bottom line: Start with a 529, fund it early, and you capture tax breaks, low fees, and an exit strategy no other account matches.

2. Roth IRA: your flexible backup plan

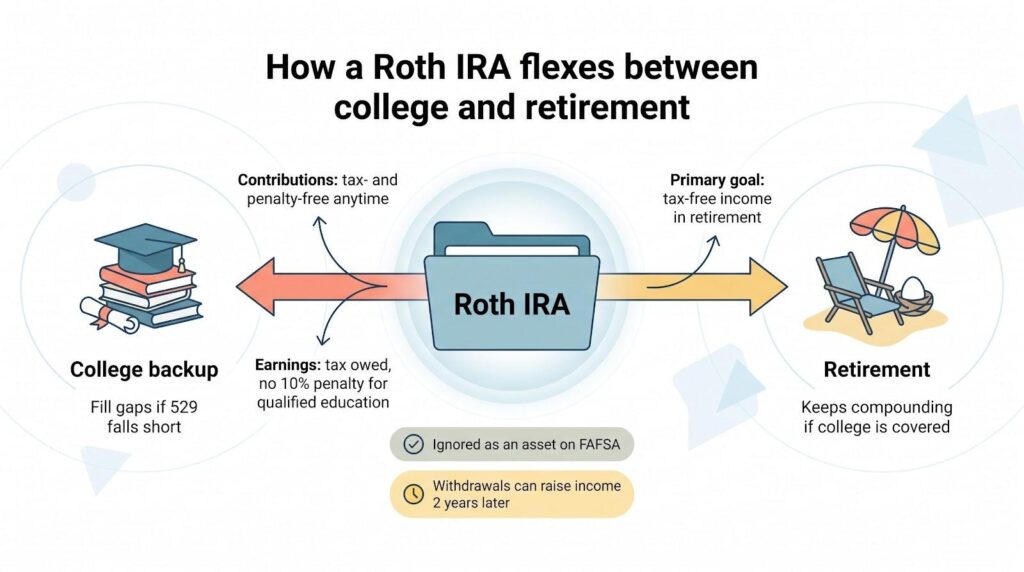

Retirement account or college fund? With a Roth IRA, it can serve both roles. You contribute after-tax dollars, let them grow tax-free, and later decide whether the money covers Chem 101 or your own beach retirement.

You set the timeline. Contributions (your original dollars) can be withdrawn anytime for any reason—no tax, no penalty. If tuition bills arrive before age 59½, you may also tap earnings without the 10 percent early-withdrawal penalty as long as the money pays qualified higher-education costs. Taxes on those earnings still apply, but skipping the penalty keeps more in your pocket.

FAFSA barely notices a Roth. Assets in retirement accounts are ignored when colleges run the aid calculation, so saving here does not hurt need-based aid. Timing still matters: a large Roth withdrawal raises adjusted gross income two years later, which can reduce aid in later semesters. Many parents wait until junior year to withdraw so the impact shows up after graduation.

Annual caps keep a Roth from replacing a 529. In 2026 you can contribute up to $7,500 per adult under age 50, far below projected tuition. High-earning couples may phase out of direct contributions. The workaround, a “backdoor” Roth conversion, survives but adds tax steps best handled with a professional.

Used wisely, a Roth IRA acts as a pressure valve. If scholarships cover college, the account keeps compounding for retirement. If costs outrun your 529, the Roth fills the gap. That dual purpose earns it the runner-up spot on our list.

3. Custodial UGMA / UTMA: the double-edged gift

Open a custodial account and you give your child more than money; you hand them full legal ownership the day they turn 21 in New York. That single fact shapes every pro and con.

On the plus side, the rules are simple. No contribution limits, no penalty for non-education spending, and no menu restrictions. You can invest in index funds, individual stocks, even the teen’s favorite sneaker company. Modest dividends and gains stay under the annual “kiddie-tax” allowance, so a small balance grows with minimal friction.

Scale it up and flaws appear. Earnings above roughly two thousand dollars a year get taxed at your bracket, erasing the advantage. FAFSA treats the account as the student’s money and expects up to twenty cents of every dollar to cover tuition, far harsher than the 529’s five-cent bite. Once your newly minted adult takes control, you lose veto power over a car purchase or a mid-semester trip.

For families certain they will not qualify for need-based aid, a modest UTMA can still work. Grandparents often like its flexibility for birthday checks. Parents who want to teach investing give a teenager real ownership in the market with guardrails that lift only when the child is legally grown.

Keep balances in perspective. Use the 529 for heavy lifting, rely on a Roth for back-up, and treat the custodial account as a learning lab or “whatever-life-brings” fund. If junior shifts the money to a food-truck start-up instead of freshman year, it will not wreck the college plan you built over two decades.

4. Prepaid tuition plans: lock in tomorrow’s price today

Picture buying four years of tuition now and never worrying about how fast the sticker climbs. That is the core promise of a prepaid plan.

Instead of owning mutual funds, you buy future credits. When your child enrolls at a participating college, those credits cover tuition at the rate in effect that term. No market swings, no second-guessing asset mixes.

Risk and reward flip from a 529. You shed investment volatility but also give up the chance to beat tuition inflation. If the stock market returns eight percent while tuition rises only four, you leave growth behind. During difficult markets, though, the guarantee feels comforting.

Flexibility is the trade-off. Most state programs limit you to that state’s public campuses. New Yorkers interested in prepaid look to the Private College 529 Plan, a consortium of more than three hundred private schools nationwide. Your student can choose any member college, but if they pick a non-member, you receive your contributions back (usually with little growth). No state tax deduction applies because New York does not sponsor the plan.

Where does a prepaid fit? It works for families certain of a private-college path and nervous about stock-market swings. Everyone else often gains more by staying with a low-fee 529 investment account that covers tuition, housing, and even grad school without tying you to a specific school list.

5. U.S. savings bonds: safety first, growth second

Series I and EE bonds are the tortoises of college saving. They move slowly, never lose a step, and finish where the Treasury promised.

Interest compounds every six months and is exempt from New York tax even if you skip the education break. Cash them after at least one year and the federal tax on interest also disappears, as long as your income stays below the phase-out and the money covers qualified higher-ed bills.

That safety comes with limits. You may buy only $10,000 of each series per owner per calendar year, so a couple maxing I bonds for eighteen years amasses $360,000 in face value before interest. Enough for a SUNY degree, but not enough to rival a maxed 529. Redeeming within five years costs three months of growth, a mild sting but a penalty all the same.

Bonds help with timing risk. Parents of high-school juniors often shift a slice of 529 money into a plan’s cash option or into fresh I bonds to lock in the bill due in two years. They trade market upside for guaranteed principal, exactly what these bonds provide.

Use them as a stabilizer, not the whole portfolio. Pair a modest ladder of I bonds with your 529 and Roth, and you can step into senior year knowing at least one bucket is immune to bear markets. That peace of mind keeps bonds in the fifth slot yet first for sleep quality when volatility spikes.

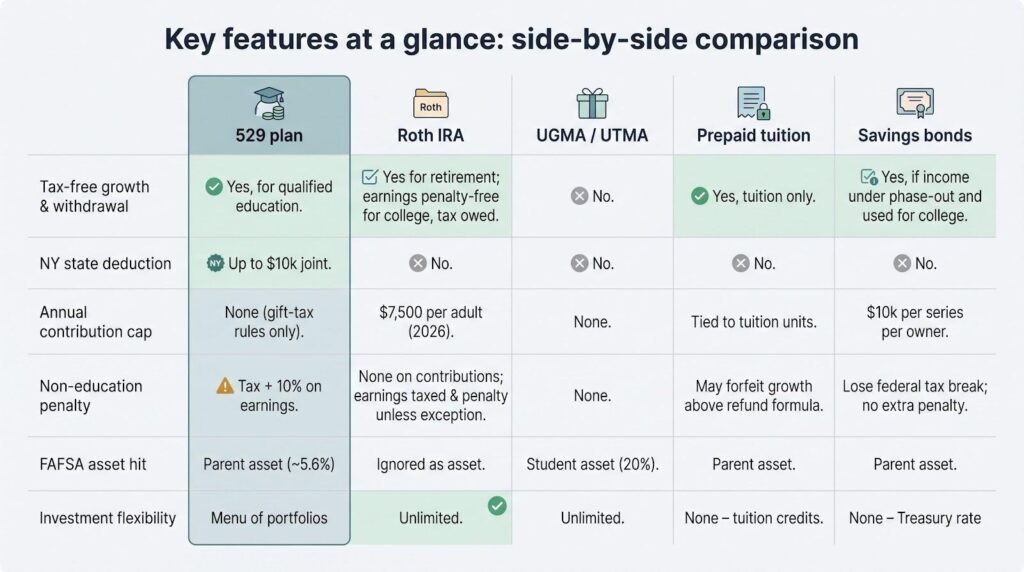

Key features at a glance

Before we return to the narrative, here is a quick side-by-side snapshot of the five vehicles. Scan the rows to see why the 529 often tops the list and where each alternative has a unique edge.

| Feature | 529 plan | Roth IRA | UGMA/UTMA | Prepaid tuition | Savings bonds |

| Tax-free growth & withdrawal | Yes, for qualified education | Yes, for retirement; penalty-free earnings for college (tax owed) | No | Yes, tuition only | Yes, if income under phase-out and used for college |

| NY state deduction | Up to $10k joint | No | No | No | No |

| Annual contribution cap | None (gift-tax rules only) | $7,500 per adult (2026) | None | Tied to tuition units | $10k per series per owner |

| Non-education penalty | Income tax + 10% on earnings | None on contributions; earnings taxed and penalty unless exception | None | Forfeit growth above refund formula | Lose federal tax break; no extra penalty |

| FAFSA asset hit | Parent asset (~5.6%) | Ignored | Student asset (20%) | Parent asset | Parent asset |

| Investment flexibility | Menu of portfolios | Unlimited | Unlimited | None (tuition credits) | None (Treasury rate) |

Conclusion

At a glance, the 529 rules the tax column and sidesteps the aid landmine, while the Roth claims the flexibility title. Custodial accounts face the steepest aid haircut, prepaid plans trade growth for predictability, and bonds deliver calm when markets shake. Keep this matrix in mind as you head to the dollars-and-cents comparison.