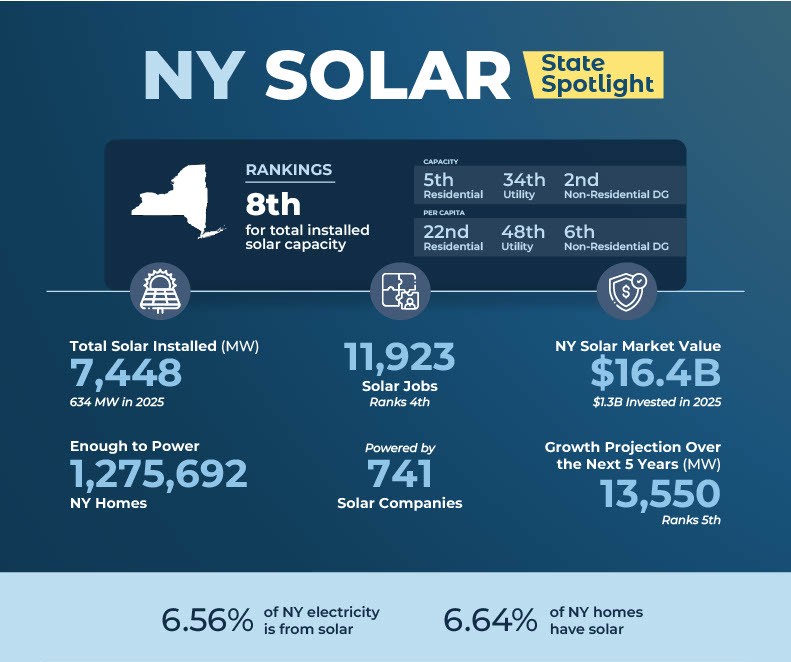

The U.S. solar industry installed 43 gigawatts (GW) of new capacity in 2025, remaining the dominant source of new capacity added to the grid for the fifth consecutive year. Solar and energy storage represent 79% of new capacity installed in the first year of the Trump Administration.

The U.S. Solar Market Insight 2025 Year in Review report released today by the Solar Energy Industries Association (SEIA) and Wood Mackenzie finds that over two-thirds of all solar capacity installed in 2025 was built in states won by President Trump. Texas, Indiana, Florida, Arizona, Ohio, Utah, and Arkansas rank among the top 10 states for solar additions in 2025.

Despite regulatory actions targeting clean energy and changing tax policy, the economics of solar remain strong as one of the few solutions that can quickly meet surging electricity demand driven by data center growth. The U.S. is expected to add 490 GW of new solar capacity by 2036, bringing cumulative installed capacity to nearly 770 GW.

“Solar and storage continue to dominate new capacity additions to the grid despite policy headwinds. American households and businesses of all sizes are demanding solar + storage because they deliver fast, affordable power to help meet rapidly rising demand,” said Darren Van’t Hof, Interim President and CEO of the Solar Energy Industries Association. “Washington must deliver policy certainty for the market to work and to keep pace with growing energy demands. Without this certainty, less solar will get built and Americans will pay the price with higher energy bills.”

“It’s clear that solar will continue to be the dominant source of new power capacity in the United States, even as gas generation continues to grow,” said Michelle Davis, head of solar at Wood Mackenzie and lead author of the report.“Strong demand growth combined with escalating costs of new gas plants will allow solar to remain competitive, even without tax credits.”

The report forecasts include scenarios showing how policy changes could impact the solar market. Final guidance on Foreign Entity of Concern provisions, the outcome of pending trade actions, and projects’ ability to secure permits will determine how much solar capacity ultimately comes online. In particular, the residential sector is facing headwinds due to changes in tax policy in 2025.

More restrictive policy will slow solar deployment, tightening overall power supply and putting upward pressure on electricity prices. Utility-scale solar is one the most cost-effective forms of new energy generation, and home solar and battery storage remains one of the few ways Americans can take control of their energy bills.

The first year of the Trump Administration was a monumental year for the domestic solar and storage manufacturing industry. With the opening of a wafer manufacturing facility in Q3, the United States now has the capacity to produce every major component of the solar supply chain. In 2025, cell production capacity continued to grow and module manufacturing increased more than 50% with 65.5 GW of capacity online.

Texas continued its dominance as the fastest-growing solar market, leading all states with 11 GW of new installations. In total, 11 states set new annual installation records in 2025, and 12 states added over 1 GW of new solar capacity. In particular, deployment in Indiana and Utah has skyrocketed, with Indiana deploying nearly 3 GW, up from 1.6 GW in 2024.

Learn more at seia.org/smi.